Introduction: In the world of mortgage financing, the term “Conventional Non-Conforming Loan” may sound complex, but understanding its intricacies can be a game-changer for your homebuying or refinancing journey. This unique mortgage option offers flexibility and opportunities for those who may not fit within the traditional lending criteria. In this in-depth guide, we will unravel the concept of Conventional Non-Conforming Loans, providing insights into what they are, who they benefit, and the key considerations you should be aware of. Join us as we explore the possibilities and potential pitfalls of this financial tool, empowering you to make informed decisions that best suit your housing needs and financial goals.

What Is a Nonconforming Mortgage?

Noncompliant mortgages are mortgages that cannot be sold because they do not meet the guidelines of government-sponsored enterprises (GSEs) such as Fannie Mae and Freddie Mac. GSE policies consist of, among other things, maximum loan amounts, eligible properties, down payment requirements, and credit requirements. Nonconforming loans are high-value mortgage loans and loans made to borrowers who are not typically eligible for Fannie Mae or Freddie Mac guaranteed loans. These loans serve as part of a private lender’s investment portfolio. Unlike traditional mortgages, there is no bulk resale.

Nonconforming loans are loans that do not meet Fannie Mae and Freddie Mac’s purchase criteria. Fannie Mae and Freddie Mac are government-funded companies that invest in mortgages. Rules regarding the types of mortgages Fannie Mae and Freddie Mac may purchase are provided by the Federal Housing Finance Agency (FHFA). There are two main reasons a loan is not compliant. Either it does not meet the requirements set by the FHFA or the loan is too large to be considered a compliant loan.

Nonconforming mortgages can be contrasted with conforming mortgages.

Understanding Nonconforming Mortgages

A non-compliant mortgage isn’t bad credit in the sense that it’s risky or overly complicated. Financial institutions do not like it because it is difficult to sell because it does not comply with GSE guidelines. Because of this, banks usually charge higher interest rates on non-compliant loans.

Most mortgages are initially written by commercial banks but often end up in the Fannie Mae and Freddie Mac portfolios. These two GSEs purchase loans from banks and package them into mortgage-backed securities (MBS) that are sold on the secondary market. An MBS is a type of asset-backed security (ABS) backed by a series of mortgages from regulated and licensed financial institutions. There are private finance companies that buy, package, and resell MBS, but Fannie and Freddie are his two biggest buyers.

The bank will use the proceeds from the mortgage sale to provide a new loan at the current interest rate. But Fannie Mae and Freddie Mac can’t just buy mortgage products. Two of her GSEs have federal restrictions on credit purchases that are considered relatively risk-free. These loans are mortgage-friendly and banks like them simply because they are easy to sell.

In contrast, mortgages that Fannie Mae and Freddie Mac cannot afford are inherently riskier for banks. These hard-to-sell loans should remain in the bank’s portfolio or be sold to a company that specializes in the secondary market for non-compliant loans.

Types of Nonconforming Mortgages

The borrower’s circumstances and types of loans that Fanny and Freddy consider noncompliant vary.

The most common non-compliant mortgages, often called jumbo mortgages, are loans written at higher amounts than the Fannie Mae or Freddie Mac limits. In 2022, that limit is $647,200 in most U.S. counties but could be as high as $970,800 in some high-cost areas such as New York City and San Francisco.

Mortgages don’t have to be huge to be non-compliant. Even small deposits can trigger false statuses. Thresholds vary but are 10% for traditional mortgages and just 3% for Federal Housing Administration (FHA) loans.

Another factor is the buyer’s debt to income (DTI) ratio. This generally cannot exceed 43% to qualify as a compliant loan.

A credit score of 660 or higher is also usually required.

The property type can also determine if a mortgage is non-compliant. For example, condo buyers are often tripped up to learning that their dream villa is not compliant because it is considered out of warranty. This includes condominium associations where a single entity, such as a developer, owns 10% or more of the unit. Other pitfalls include if the unit is largely unoccupied by an owner, more than 25% of the square footage is used for commercial purposes, or the Homeowners Association (HOA) has filed a lawsuit. There are cases.

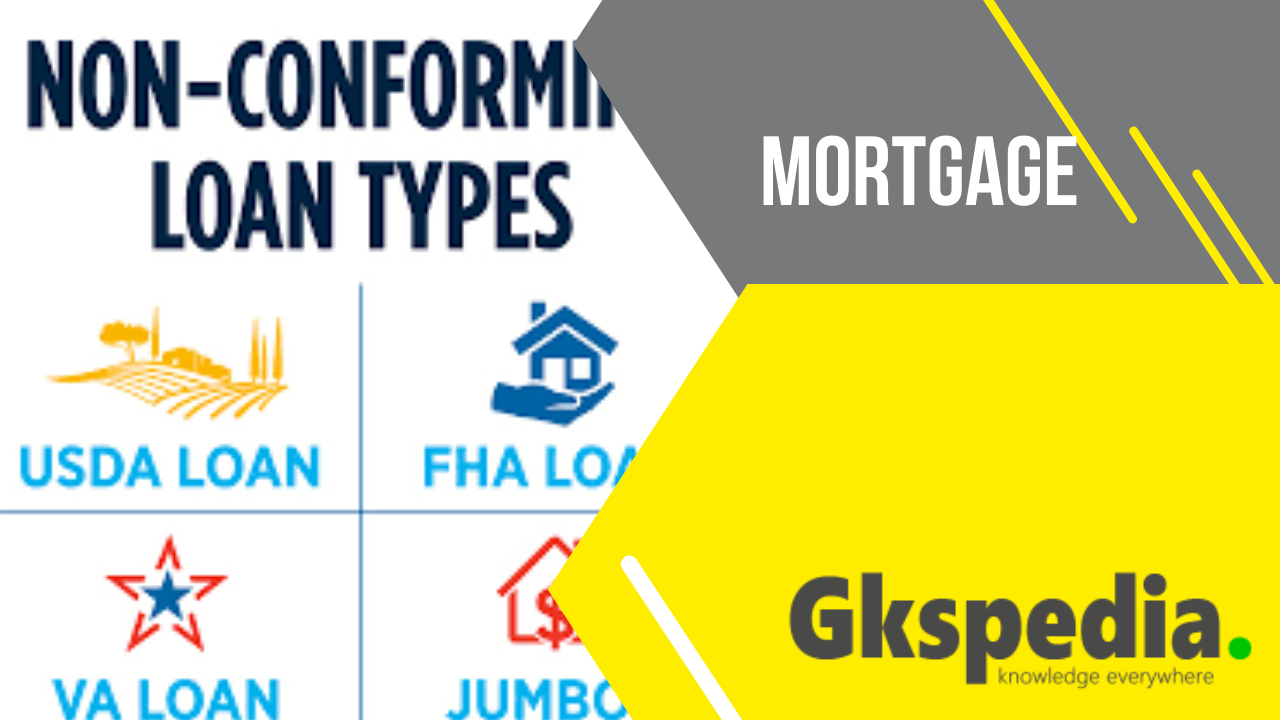

Government-Backed Loans

A government-backed loan is a federally backed loan. In other words, the government bears the bills and helps cover losses due to loan defaults. Government-backed loans are less risky for investors. As a result, the buyer’s down payment and credit score can be lowered. However, you and your home must meet certain criteria to qualify for a government-backed loan.VA loans, USDA loans, and FHA loans are the three forms of government-backed loans available. Each loan kind has its own set of requirements for eligibility.

VA Loans: VA Loans are loans for eligible military personnel, veterans, and their spouses. You must meet minimum service requirements or be the surviving spouse of a service member who died in service or died as a result of disability. You can purchase a home with a VA loan with no money down. You can also refinance 100% of the value of a home with a minimum credit rating of 620. The VA does not set specific minimum credit requirements, but lenders can set their own guidelines. Rocket Mortgage requires a median FICO® score of 580 or higher. The Department of Veterans Affairs guarantees loans to veterans.

FHA Loan: With an FHA Loan, you can buy a home at just 3.5% off. A median credit score of 580 or higher and a qualifying debt-to-income (DTI) ratio are required. If your average FICO® score is 620 or higher, your DTI may be slightly higher. The Federal Housing Administration insures FHA loans.

USDA Loans: USDA loans are loans for buyers who want to buy a home in a rural or suburban area. Your home must be in an area that the USDA considers sufficiently rural. Also, you cannot earn more than 115% of the county’s median income. Also, you can’t turn your house into a farm. You can buy a home with a $0 down payment and an average credit score of just 640. USDA loans are not presently available from Rocket Mortgage.

Nonconforming loan requirements

Especially for jumbo loans, lenders can expect borrowers to find higher down payments, higher credit scores, higher cash reserves, and/or lower DTI ratios to justify the size of the loans. At least he can expect to pay a 20% down payment if he plans to resort to non-compliant loans. You can find out the interest rates for jumbo loans here.

Noncompliant loans may also be available to borrowers who have recently filed for bankruptcy and may be excluded from compliant loans.

There are three common reasons a borrower is not compliant with his loan:

Loan Size: If in most of the United States he owes $647,200 or more, or in high-cost areas like Hawaii he owes $970,800 or more, a ineligible loan is required. No more than that and a matching loan will suffice.

Credit Score: If you have credit issues and your FICO score is less than 630, you may not be eligible for a compliant loan. Federal Housing Administration mortgages are a popular choice for borrowers with lower credit ratings. With an FHA loan, the down payment can be as low as 3.5% for him. One downside: FHA loans are more expensive than conforming loans due to higher mortgage insurance premiums. High DTI Ratio: Even if you’re kicked out of Fanny and Freddy’s territory because of your debt, you may still be able to get a non-compliant loan, known as an FHA mortgage or non-QM mortgage.

Benefits Of Non-Conforming Loans

Benefits of taking a non-conforming loan include:

Lower Down Payment Requirements: Non-compliant government-sponsored loans typically have lower down payment requirements than traditional loans. If you qualify for a USDA or VA loan, you can buy a home with a 0% discount.

Greater Credit Limits: If you’re looking to buy an expensive property, you may be forced to opt for a non-compliant jumbo loan. Jumbo loans give you access to higher credit limits than matching loans.

Other Types of Real Estate: Depending on the type of loan you take, a non-compliant loan can purchase types of real estate that a compliant loan cannot acquire. Poor credit score: Many lenders offer customized non-compliant lending solutions to people with negative credit report scores. For example, if you have bankruptcy on your credit report, you may not be able to get a compliant loan for several years. However, lenders may be able to provide customized non-compliant solutions. Note that in most cases you will pay more interest on these loans.

How Non-Conforming Loans Work

Loan amounts are higher for non-compliant loans and the required documentation is more extensive. There may be some other differences as well.

Deposits can be large.

Your credit score threshold may increase.

The debt-to-income ratio is stable.

A large cash reserve may be required. Interest rates may rise.

Closing costs and fees can be high.

There are many instances where your only option is to obtain a non-compliant loan. If you want to buy a house with no down payment, you can if you qualify for a VA loan (one of the most important benefits of military service) or if you live in a rural area and he qualifies for a USDA loan. FHA loans are ideal for customers who want a home loan with low credit requirements. On the other end of the spectrum, lenders require you to take out a jumbo non-compliant loan if you want to buy a more expensive home.

In addition, non-conforming loans are ideal for people who have a negative mark on their credit score but want to buy or refinance a home. Many lenders offer individualized solutions to individuals who are ineligible for compliant loans due to bankruptcy or other negative impacts on their credit scores. If you don’t qualify for both a government-backed loan and a compliant traditional loan, a non-compliant loan may be for you.

Loan Amounts

Non-compliant mortgage amounts vary by year and region. They range from $548,250 for him in 2021 to over $647,200 for 2022. Where housing costs are much higher, the number of nonconforming mortgages in 2022 will exceed $970,800. This is up from $822,375 in 2021.

Documentation

Be prepared to give the lender a lot of information when seeking credit outside of standard channels. You must submit multi-year income tax returns, payslips, and bank statements. If you have other assets or items of value, we may ask you to value them. Lenders look for materials that may relate to your wealth, creditworthiness, or income to determine if you are safe enough to provide a loan.

The Down Payment

Some lenders only accept a 10% down payment, but this is not common. Often, private mortgage insurance with as little as a 10% down payment is required. Many lenders require a down payment of around 20%, but the exact amount depends on the details of the loan.

Your Credit Score

You need a credit score of at least 680 to get this type of loan. Your credit rating also affects the interest you pay. A better credit rating can save you money over the life of the loan.

Debt-to-Income Ratio

Lenders aim for a debt-to-income ratio of 40% or less but may settle for more if large amounts of cash are available.

Cash Reserves

Most non-compliant jumbo lenders should have a reasonable amount of cash on hand as the size of their loans can result in significant losses in the event of a foreclosure. The amount is set by each lender but is often the equivalent of a year’s mortgage payments.

Interest Rate

Interest rates on non-compliant loans are almost always slightly higher than on low-value loans. Lenders compete to keep interest rates as low as possible while making money.

Closing Costs and Fees

Fees are calculated as a percentage of the mortgage balance, so non-compliant mortgages have higher surrender costs and fees. This type of mortgage also has additional closing costs such as B. A series of property appraisals.

Why you might choose a non-conforming loan over a conforming mortgage

Common sense makes it clear that you should care if the non-compliant loan is more expensive than the non-compliant loan. Many people think non-compliant loans are for low credit borrowers. This is not necessarily the case.

In many cases, the only reason a loan is noncompliant is its size. In fact, these “jumbo” mortgages may have higher interest rates than matching mortgages. So you might choose a non-compliant loan just to get a more expensive home. However, these loans can be financed by checking your income differently or by avoiding waiting times after a significant event such as bankruptcy or foreclosure.