Introduction: When it comes to financial planning for retirement or unlocking the equity in your home, an Adjustable Rate Reverse Mortgage is an option that warrants a closer look. This financial tool offers unique benefits but also comes with certain risks and considerations that need to be carefully weighed. In this comprehensive guide, we will delve into the world of Adjustable Rate Reverse Mortgages, exploring their advantages, potential drawbacks, and helping you make an informed decision about whether this option aligns with your financial goals. Join us as we navigate the complexities of this mortgage type and shed light on how it can impact your retirement and financial well-being.

With a malleable rate rear mortgage, the interest rate can change and conceivably increase over the life of the loan. The advanced the interest rate, the briskly the top balance grows so a malleable rate rear mortgage exposes the borrower to further threats than a fixed rate loan. The borrower can choose between a mortgage that adjusts on a yearly base or on a periodic base, with the periodic malleable rate rear mortgage being the most popular.

The interest rate for a malleable rate rear mortgage is comprised of two factors the periphery and the indicator. To calculate the interest rate, you add the periphery to the indicator. For illustration, if the periphery is2.500 and the indicator is1.000, the interest rate for your rear mortgage is3.500.

The periphery is a set interest rate quantum that doesn’t change over the term of the rear mortgage. The periphery is generally2.0-3.0. The periphery is determined by the lender and subject to concession with the borrower.

The indicator is a beginning interest rate that can change over time. Rear mortgages attained prior to June 2020 generally use LIBOR as the indicator while rear mortgages after June 2020 generally use the 30-day average SOFR( Secured Overnight Financing Rate). Simply put, SOFR and LIBOR represent the interest rate that banks charge each other to adopt plutocrats and change grounded on movements in frugality. The values for SOFR and LIBOR change but are the same for all banks.

LIBOR is being excluded after 2021 and utmost LIBOR- grounded rear mortgages will transition to SOFR. We recommend that you review your rear mortgage documents to learn how your rate is calculated when LIBOR isn’t published.

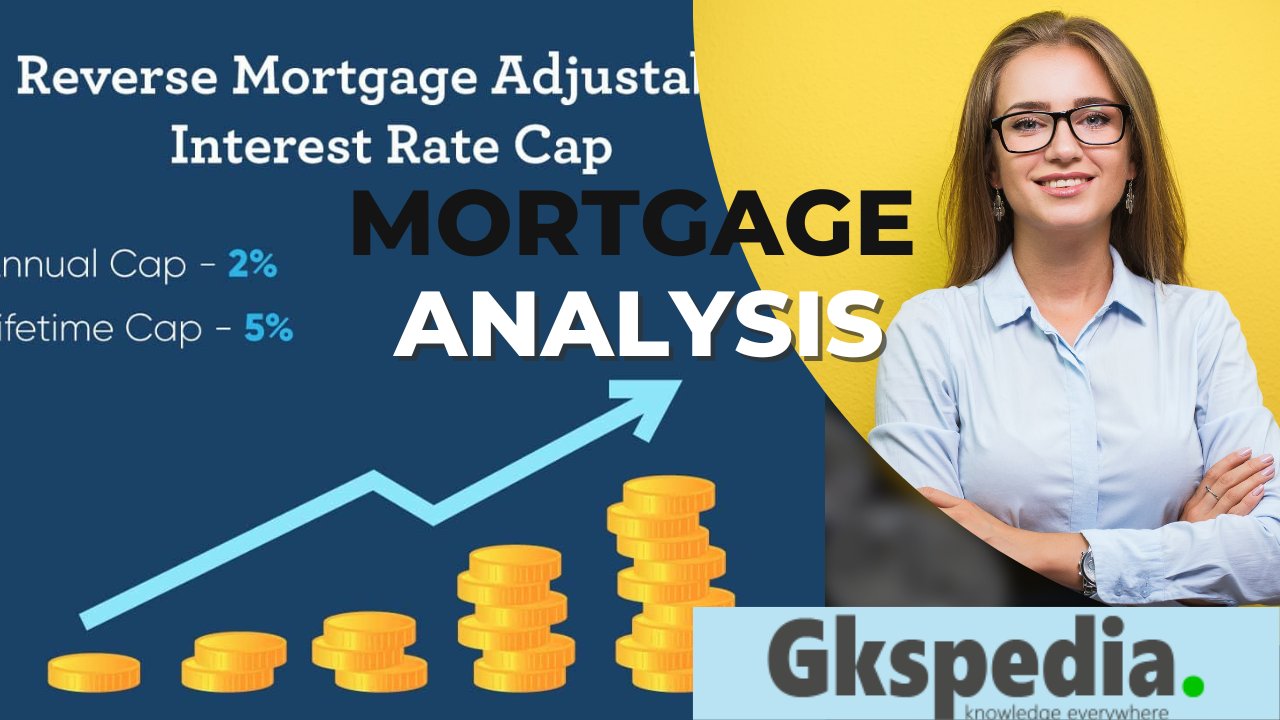

The interest rate for a malleable rate rear mortgage is calculated on a yearly or periodic base for the wholeness of the loan and changes with any oscillations in the index. However, your interest rate increases, and the loan balance increases briskly over time because you’re adding further interest expenditure to the loan, If the indicator increases. The interest rate for a malleable rate rear mortgage also has a life cap which limits how important it can increase over the term of the mortgage. The typical life cap for a malleable rate rear mortgage is5.0 which means the interest rate over the life of the loan can not exceed the original rate by further than5.0.

Disbursement Options for a malleable Rate Rear Mortgage

The maximum quantum of proceeds the borrower is suitable to admit at closing with a malleable rate rear mortgage is equal to or lesser than a fixed rate rear mortgage( depending on the borrower’s age), plus the borrower has further options for how and when they take disbursements over the life of the loan. also, with a malleable rate rear mortgage, the borrower is suitable to adopt further over the life of the loan as compared to a fixed rate rear mortgage.

With the malleable rate option, the borrower receives an outspoken disbursement when the mortgage closes and is suitable to take fresh disbursements after staying a time. The maximum outspoken disbursement equals roughly 60 or lower than the original star limit. The borrower has to stay twelve months after the mortgage closes to be suitable to pierce the remaining available loan proceeds, up to the original star limit, either through another lump sum disbursement, yearly disbursements, or through a line of credit.

Pros

The initial interest rate for variable rate reverse mortgages is lower than the interest rate for fixed-rate reverse mortgages

Lower interest rates reduce interest expense and slow the growth of your main mortgage balance.

Variable rate reverse mortgages offer more payment options and give borrowers more financial flexibility

Offers borrowers significantly higher gross income compared to fixed-rate reverse mortgages.

A variable rate reverse mortgage lets you borrow more money over the long term

Cons

Interest rates on floating rate reverse mortgages can fluctuate and potentially rise, exposing the borrower to greater risk.

Higher interest rates mean higher interest payments, and major mortgage balances grow rapidly over time.

The ability to increase your home equity with a variable rate reverse mortgage means that your home equity may be less at the end of your loan.

Fewer assets mean less income you or your heirs will receive after you sell the property or pay off your reverse mortgage.